Capgemini has succeeded with its offer to purchase Altran. The company has secured 53.4% of Altran’s capital. Capgemini will reopen the tend offer from January 28 to February 10.

One has to admire the way Capgemini has handled the acquisition process. The company has gained control of Altran at a competitive price and become the worldwide leader of ER&D services. Also, incidentally, Capgemini will only have to spend half of the EUR 3.6bn: investors, which had been worried about Capgemini increasing its net debt by EUR 5bn (Altran brings a net debt at end of 2018 of EUR 1.4bn). Also, Elliott International will have delayed the acquisition by only two months: the impact on Altran’s attrition should have been limited.

Finally, Paul Hermelin, the CEO of Capgemini leaves the company (mid-May) on a very positive note, having transformed the firm very significantly from a USD 8bn firm (that was almost killed by the acquisition of Ernst & Young Consulting) to a USD 19bn leader that has well managed its transformation toward Indian offshoring and digital.

The picture is not all gloomy: Capgemini will not take operational control of Altran before the Paris Court of Appeal provides its ruling, by Mid-March. In the meantime, Capgemini will not be able to derive commercial and cost synergies and Altran will keep on operating as standalone.

Also, we are betting that Capgemini will want to gain full control of Altran and will launch another tender when its 18-month no-offer period is passed. The story of the acquisition of Altran is far from over. However, one must admit that Hermelin mastered the acquisition process and did not overpay for Altran.

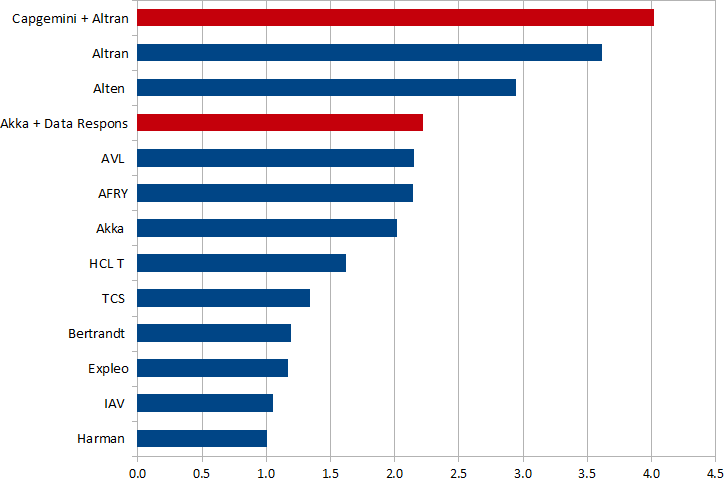

Ranking of ER&D Services' Top Vendors, by 2019 Revenues (USD bn)